40 years

We are continuing our line of reviews of the IT industry companies stocks, and Intel surely cannot be left aside. See the chart below.

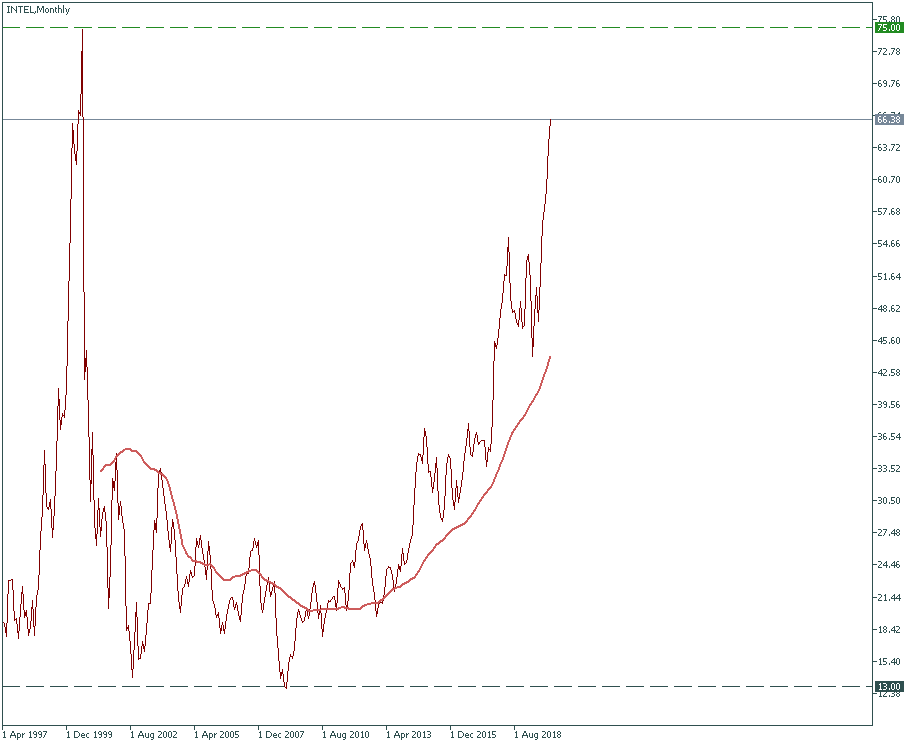

That’s what the 40-year story looks like. Of course, you immediately see the peak of the year 2000 asking “What happened there?”. You will be surprised to know – nothing as extraordinary as the chart looks like. Although the entire IT industry suffered from the crisis that year and most of the stocks in this market sector slumped double-digit, not all of them were so quick to fall. Intel’s case is an overlap of a global factor, industry-specific factor, and the company’s own decision-making. Which resulted in a very dramatic case, as you can see. Let’s take them one by one to see how good the outlook for this stock is now.

Stock value, sales, earnings and business model

The 2000-s economic recession set the background for the performance. As the IT industry in terms of its market valuation relies heavily on the sales projections and future demand, there was nothing positive in this regard in the said period. American and European markets promised no bright future at that time, so the entire IT industry expected no good sales in the early 2000-s. Hence, the majority of the IT companies, including Intel, saw their stock drop in value.

At an industry level, the IT sector was going through a transformation. The PC era was going to enter its final stages at that time because its customer base was starting to erode – people were favoring portable devices more and more. Hence, desktop personal computers, to which Intel was supplying a big chunk of its microprocessors, were gradually giving away the market share to new era products. Intel had problems to adapt to that, therefore the damage exacted on its sales by the global crisis was doubled and doomed to be not a single strike of misfortune, but a first serious breakout of a chronic miscalculation.

And lastly, being an industry leader at its time, Intel was used to enjoy its sales very much due to the vast size of every single sale that brought a good margin. When mobile devices such as (and primarily) Apple’s iPhone got introduced to the audience, Intel had an opportunity to re-focus its capacities to fit this emerging sector and particularly to start producing chips of a new standard to fit into Apple’s production line. But Intel turned down that option because it saw little reason in re-structuring its PC- chips-market-domination strategy and to venture into something new. How can a small device merely around $1000 in price give enough margin to return the costs of the business based on selling parts to desktops costing so much more? Apparently, this question should have been answered with more enthusiasm by Intel's top managers 15 years ago. But it wasn’t. That’s why Intel is having hard times getting out of trouble now, with contracting customer base, lagging behind the technological standards for chips production and needing to fire more than 10000 employees from time to time (like in 2016).

So what is it now?

Currently, Intel’s stock trades at the level of $66 per share. Since the 2000-s shock, where it peaked at $75, it made almost a complete recovery. And that is exactly what is worrying. Such periods of parabolic growth are often precursors of a cycle change within the industry: exactly the same happened right before the year 2000.

How should we mark the checkpoints then? On a daily chart, $70 should serve as a reliable resistance checking the upward movement. If it is crossed, psychologically the market will have little doubt to reach its all-time high at $75 for this stock. Otherwise, $64 is the level that supports the recent consolidation area. Primarily, the price has all the reason to go down to it, as it has been trading too long above the 50-MA – that normally doesn’t end well for the price. Secondarily, if this support is reached, there will be full strategic potential for the price to drop to $43. Although it seems like a doomsday scenario right now, it might not be that unrealistic – remember 2000?

Any final words?

Yes, the final word with this stock is “be careful”. Intel's business seems to be on a shaky path. Although the company’s top managers have been implementing measures to restructure the business and adapt it to the industry and customer demands better, the mid-term intuition says “sell”, while the long-term suggests “you can buy, but prepare for surprises”. But it makes sense to try it anyways - at least one share does not cost as much as Amazon.

TRY IT